Interview with Tracy Kitten before EMV was a story in the USA

Category: EMV

The Card Was and Is Only a Credential Carrier

Cash is here to stay – cards are the true dinosaurs

This question of the extinction of the payment card is misleading.

What is a payment card? It is the carrier of a set of credentials, A means of Identification offering financial Attributes capable of being authenticated by a party seeking to sell something to the individual or entity presenting the credential as a mechanism to assure payment.

Back when credit cards were designed, the goal was to offer merchants a guarantee of payment and anonymous consumers a means of paying. Behind this means of payment, a financial institution, the issuer, provides the consumer with a “Line of Credit”.

On the merchant side, another financial institution buys these guaranteed receivables from the merchant and charges the merchant a “merchant discount”. Later that day the Issuing Institution advances payment to the Acquiring Institution based on an agreed set of terms and operating rules. Terms and conditions the involved financial institutions collectively agreed upon.

For this method of payment to be effective, a large number of consumers and merchants had to agree to participate; hence the financial institutions came together and formed what we now know as MasterCard and Visa.

Given the state of technology at the time it was essential this new mechanism work without the burden and expense associated with the merchant, supported by the acquirer, contacting the issuer to receive approval, or, in stronger terms be assured of a guarantee of payment. To achieve this result, the merchant needed something to acquire the necessary information to submit a request for payment. For both the merchants and financial institutions,, there had to be a means of authentication. Designed to assure the responsible parties of the authenticity of the person or entity to present their payment credentials.

To accomplish this goal, just like with money, physical security features are integrated into the payment card designed to allow the merchant to authenticate the uniqueness of the card carrying the payment credential, thus assuring the merchant of the authenticity of the card.

To accomplish this goal, just like with money, physical security features are integrated into the payment card designed to allow the merchant to authenticate the uniqueness of the card carrying the payment credential, thus assuring the merchant of the authenticity of the card.

Overtime criminals successfully counterfeited these security features.

As these features were compromised additional features had to be added.

Today, a computer has been embedded inside the card, in order to assure the authenticity of the payment card credentials being presented to the merchant.

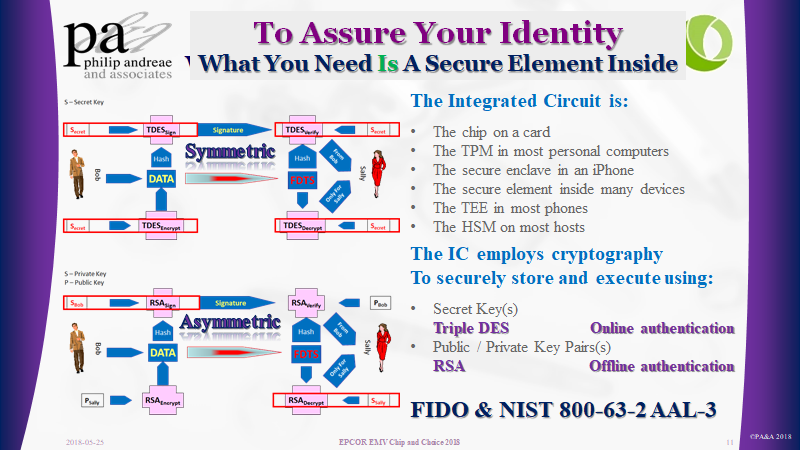

These computers embedded onto the front of a payment card exploit the power of cryptography. Cryptographic certificates and digital signatures are created by and for these computers, allowing:

-

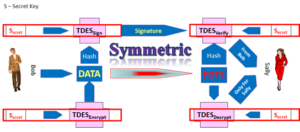

- The Issuer (symmetric cryptography) to support Online Authentication

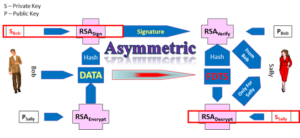

- The merchant (asymmetric cryptography) to support Offline Data Authentication

These two mechanisms prove to the merchant and issuer that the card is unique and the data, credentials, and digital signature it contains or produces are authentic.

Once all the merchants have are capable of reading the data from the chip card, the security features of the card become redundant.

As these features become redundant and the merchants embrace Near Field Communications, based on the ISO 14443 standard, the issuer can replace the card form factor with anything equipped with the necessary computational capabilities and ability to communicate with the terminal over the NFC interface.

This is exactly what Apple Pay and Google Pay have done. They replaced the card with a device. Yes, the Payment Card may become redundant. But, the Payment Credentials they contain, remain.

What we know as card payments, is fundamentally an account-based solution. Money, through the defined settlement process, ultimately move from the line of credit or deposit account of the buyer, through a series of accounts with the participating financial institutions, to the account of the merchant.

Card-based credential payments

simply become

Device-based credential payments

EMVCo Good or Evil

https://www.securepaymentspartnership.com/wp-content/uploads/2019/12/Payment_Insecurity_Final.pdf

In 1993, I was asked by the then CEO of Europay International to establish a relationship with Mastercard, and Visa focused on developing the specifications necessary to assure the interoperability of chip card-based security for credit and debit payment cards. The result published in 1996 was the “EMV Integrated Circuit Card Specifications for Payment Systems.”

From these humble beginnings, EMVCo has emerged as a key organization in managing the standards behind card payment systems. In the white paper Payment Insecurity, commissioned by the Secure Payment Partnership, the author reminds us of the difference between standards managed by an open body and those tightly controlled by an exclusive group of competitors. One wonders if the owners of EMVCo will listen and strive to open up their membership or continue to use this entity to protect their proprietary interests.

In the introduction, the author speaks of a series of questions he intends to address. The first question of the paper

Is EMVCo furthering the entire U.S. payments industry or simply protecting Visa and Mastercard’s market share? page 5

begs the question, why limit the discussion to the USA?

This American only focus is driven by the desires of the Unaffiliated Debit Networks and a set of merchants. The paper ignores fundamental and, yes, anti-competitive elements of the EMV specification – the AID or the Application Identifier. It was and is directly related to the Brand responsible for the underlining technology incorporated into the Chip.

I then read the following complaint and am driven to ask how the consumer interpreted the prior Debit versus Credit prompts.

Visa’s response to this solution was to require merchants to display to consumers a choice between “Visa Debit” and “U.S.

Debit” at checkout. – page 13

In essence, what Visa required was simple, the terminal should comply with the EMV specification for “application selection,” key and inherent in the multi-application design of EMV and the underlining ISO 7816.

Moving further into the document in Section 6.1, the author attempts to document the history leading to the creation of EMVCo. As one of the founding members, the author’s sources were not involved and did not understand the history.

First, only France had a smart card solution designed to address Credit and Debit card fraud. They referred to their implementation as B Zero Prime.

Second, the UK in 1995 was driven by Visa to embrace an earlier version of the Visa specifications adapted to the unique requirements of the UK market and branded UKIS. UKIS and the unique UK requirements are responsible for changing many of the shall’s in the EMV 2.0 version of the specifications to should’s in the EMV 3.0 version. This accommodation was the result of legacy limitation within the X25 network the United Kingdom depended on for card authorizations.

To further identify issues with his record of history, the statement on page 22

EMVCo developed standards for chip cards that could work with credit, debit and stored-value cards

It is fair to suggest EMV attempted to incorporate Stored-Value cards in the specification. But as a result of the competitive realities of Europay’s Clip, Mastercard’s Mondex, and Visa Visa Cash stored value solutions, they agreed to exclude stored value cards from the specifications.

It then goes on to suggest EMV compromised and offered a Signature option. There was not a compromise; it was intentional. The goal, afford the Issuer the ability to determine, by Cardholder, which cardholder verification method they could be configured for. One need was to address issues of the disabled, e.g., the Blind.

Debit Routing as a result of the Durbin amendment. One might wonder why EMV did not consider this idea of multiple networks associated with a card.

EMVCo was unable and unwilling to resolve the lack of a debit AID because EMV was never designed for the U.S. market.

I sense that there is another front coming out of the Debit Networks seeking to argue the anti-competitive nature of EMV. The paper, link below, draws me to wonder about the argumentation surrounding “Application Selection.” Please let’s get back to basics – the “AID=Brand=Payment Scheme” drives “Routing.”

On page 13, it argues consumer confusion. I would argue it ignores the past. The EMV default user prompts of “Visa Debit” and “US Debit” are no more confusing than the historic “Credit,” and “Debit” prompts. I would argue consumer confusion already existed. The EMV specification for Application Selection simply afforded the Issuer the ability to provide more descriptive prompts by employing the “Application Preferred Name” instead of the default “Application Label.”

This whole fight surrounding EMV and Payment Security is really a fight about the future of Card Payments. On one face, they argue the Payment Networks did not assure the security of the card payments to protect revenue. On the other hand, they argue EMVCo is a closed standards organization designed to protect and assure the interests of its shareholders, without consideration for the other stakeholders in the payment, e.g., the merchant.

In the end, the argument comes down to the role, definition, and control. How we structure the underlining payment transaction is what we need to talk about. Who provides the mechanism, guarantee, and support for a particular mechanism decides the rules.

The Identifier should not be the Authenticator

I was asked to look into the value of the EMV Secure Remote Commerce Specifications. In the first section they wrote:

“1.1 Background … While security of payments in the physical terminal environment have improved with the introduction of EMV specifications, there have been no such specifications for the remote commerce environment. …”

This statement caused a bit of angst. It caused me to think of the work to create SET and Visa’s efforts to promote the original version of 3D-Secure. I was further reminded of how difficult it has been to find the balance between convenience and fraud and how merchants are more worried about abandonment than they are about the cost of fraud. Ultimately, it caused me to wonder about the goal of the EMV 3-D Secure specification.

“To reflect current and future market requirements, the payments industry recognised the need to create a new 3-D Secure specification that would support app-based authentication and integration with digital wallets, as well as traditional browser-based e-commerce transactions. This led to the development and publication of the EMV® 3-D Secure – Protocol and Core Functions Specification. The specification takes into account these new payment channels and supports the delivery of industry leading security, performance and user experience.”

The keywords found in the last sentence “the delivery of industry leading security, performance and user experience” suggest these two specifications are searching to solve the same problem.

According to the Oxford dictionary

Security is

- “The state of being free from danger or threat.”

- “Procedures followed or measures taken to ensure the security of a state or organization.”

Authentication is

- “The process or action of proving or showing something to be true, genuine, or valid.”

- “Computing The process or action of verifying the identity of a user or process.“

On this same page, the authors go on to make the following statement

“… there is no common specification to address the functional interactions and transmission of data between the participants.”

This then causes me to wonder about the original ISO 8583 specification, the current ISO 20022 specification, and the subsequent concept of the three-domain model within the 3D-Secure specification. All three of these specifications define the interaction between the participants while not restricting the method of transmitting the data. It seems the authors of the SRC specifications have forgotten history. Or, are they trying to rewrite history.

At this stage, Authentication seems to the most important part of what EMV is attempting to address. But, the focus seems to be more about rewriting history that solving the fundamental problem. We seem to have this desire to take public identifiers and convert them into secrets.

“An industry transition from a dependency on Consumer entry of PAN data can be accomplished by providing an SRC specification that meets the needs of all stakeholders involved.”

These intriguing contradictions beg the question. Why did the authors of the Secure Remote Commerce specification not reference the good work of those that created the 3D-Secure specification and propose an approach unlike EMV? They all are part of the same organization!

Is the goal not to address authentication and Security of the payment transactions, be they instore or on the Internet. I would argue

We allowed the PAN, the payment card identifier, to become a means of authentication

This use of the PAN as both an identifier and an authenticator; reminds me of a hearing of the United States House Committee on Ways and Means May 17th, 2018 hearing on “Securing Americans’ Identities: The Future of the Social Security Number”.

“House Ways and Means Social Security Subcommittee Chairman Sam Johnson (R-TX) announced today that the Subcommittee will hold a hearing entitled “Securing Americans’ Identities: The Future of the Social Security Number.” The hearing will focus on the dangers of the use of the Social Security number (SSN) as both an identifier and authenticator, and examine policy considerations and possible solutions to mitigate the consequences of SSN loss or theft.”

All the witnesses and most of our members of congress accepted and understood the problem. We allowed a simple government-issued identifier to become a means of authentication, in other words, an authenticator. Like allowing the social security number and now also the PAN to become part of how we authentic someone’s identity. We caused these publically available identifiers to become valuable and sensitive PII data.

Cardholder Authentication and Consumer Device Identification

What is clear, as one continues reading the SRC specifications, is the goal is to reduce the frequency of presenting payment credentials on merchant websites.

“Minimising the number of times Consumers enter their Payment Data by enabling consistent identification of the Consumer and/or the Consumer Device”

A very different approach to what the payment schemes do with the EMV based payment process. The authors of EMV saw the PAN as public data, they architected something designed to assure the uniqueness of the card and the ability to positively verify cardholder. Card Authentication and Cardholder Verification.

Why not simply think and focus on the same architecture? Simply change the word “card” to “device” and focus on Device Authentication and Cardholder Verification or as everyone is promoting Multi-Factor Authentication. We simply need to make sure the thing is genuine and the right individual is using the thing. The thing is what the cardholder has – The “what you have” factor. Add a pin/password or better still a biometric to be the second factor the “what you know” or “what you are” factor.

EMV 3D-Secure creates the ability to exploit the “what you have” factor by offering Device fingerprint data to the issuer’s authentication process.

What You possess, What You Are, What You Claim … Your Certificates

NCCOE NIST Multi-Factor Authentication

What you Possess — The Thing

What you Are — You

Your Relationships

Responsibilities

Authority

Advice

— Secrets

My Certificates

World Wide Web Consortium

FIDO Alliance

Global Platform

The Trusted Computing Group

- EMVCo

- ISO

- ANSI

- ABA

Future interests

- Artificial Intelligence

- Machine Learning

- Nature Language Interface

- Predictive Analytics

Smart Cards with Fingerprint Scanners

Over the last couple of years the reality of fingerprint cards is a hot topic in conversation, white papers and press articles. It led me to think about the challenges and opportunities associated with this intriguing convergence of technologies.

My purpose is not to determine which solution is best or which companies are developing and selling them. My goal is simply to explore.

The first consideration begins when the card is constructed. Here we must ask the mechanical question relative to how the electronics are integrated into the strata of an ID-1 card. This then begs the question of making sure this new card conforms to the specifications dictated by Payment, Networks, Governments or other bodies who define the use of these branded cards. If we continue to think about the card manufacturing process we need to think about electronics and the use of heat in the typical lamination process or the inclusion of metallic materials used to create a particular look. One needs to think about the method of connecting the various internal components to the other electronic elements as the fingerprint scanner, antenna(s)m LEDs, batteries, the EMV chip or contact plate on the face of the card.

The second set of concerns must be related to the personalization of the card. First question is where will it be personalized? in a branch or within a bureau? How will it be personalized? With a thermal printer, laser engraver or embossing machine? Will any of the personalization processes adversely affect the electronic?. Similarly it will be appropriate to confirm whether any of the various card transport mechanisms will disrupt or damage the sensor and related electronics.

At some point in the processes the consumer must register their fingerprint and the resulting template must be instantiated into the card. How will this be done? Some speak of an in branch process. Others talk about some type of first time cardholder activation process performed when they receive the card in the mail.

Clearly there are a lot more questions the issuer, card manufacturer and personalization provider need to address. Let alone the method of making sure the cardholder knows how to use the card at the point of sale or ATM

The key question is the cost of the card, is it worth it?

EMV Light Touch

Wednesday February 27th, 2019

At Kennesaw State University

As part of Coles College of Business

Information Security Lecture

I offered the following:

What I call an EMV Light Touch

Video of the Presentation

Payment Card Security

Dual Interface Construction

When we think about the migration to contactless or Dual Interface cards it is important to have a general understanding of what goes into creating the card and the constraints one has to think about, as they work with their marketing teams to design these cards.

When we think about the migration to contactless or Dual Interface cards it is important to have a general understanding of what goes into creating the card and the constraints one has to think about, as they work with their marketing teams to design these cards.

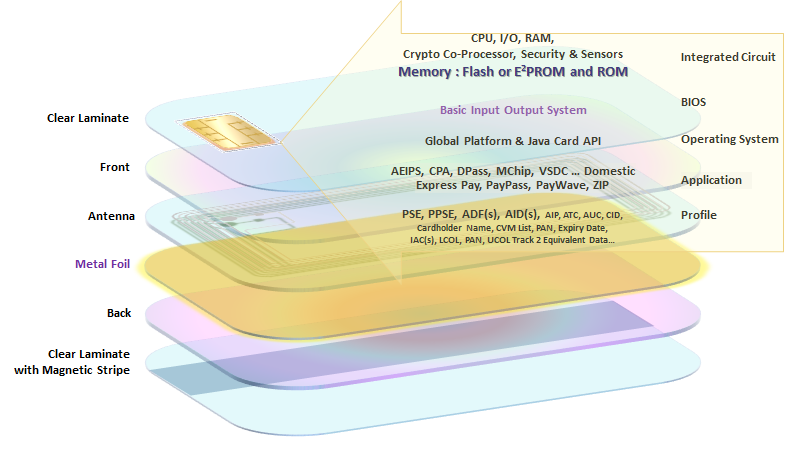

The design of a payment card involves assembling multiple of PVC into a sandwich that will be bonded and then punched out to form the card body.

- On the face of the card: a clear laminate to protect the surface

- On the back a clear laminate with the magnetic stripe affixed to it

In the middle two printed sheets

- The front

- The back

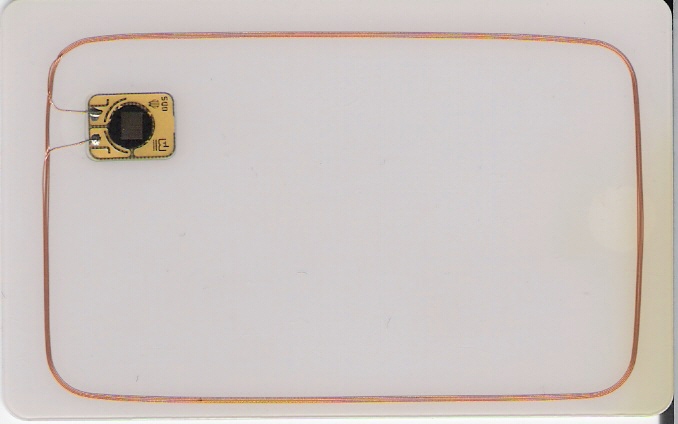

In the middle of the card body, your manufacturer will need to insert an antenna. The antenna is typically provided to the card manufacturer as an inlay, as seen on the left. The inlay is a sheet of plastic with the copper antenna, sometimes aluminum embedded within. The card manufacture will add this inlay into the middle of sandwich.

On the right is an example of a six layer card construction including one element as an example, a metal foil. This has been included given it has an impact on the effectiveness of the radio signal. More about this a little later. Using pressure and heat, the layers of the sandwich are bonded together in a process called lamination. The bonded sandwich is then run through a series of additional processes designed to create an ID-1 card as specified in the ISO 7810 specifications supplemented by the additional payment network requires, such as the signature panel and the hologram.

After quality inspection the next step is to mill and embedded chip into the card body and simultaneously assure a connection between the contacts on the back of the chip and the antenna. There are various means of connecting the chip to the antenna. These different methodologies for connecting the chip to the antenna is a specific skill and is the responsibility of your card manufacturer. Look to your manufacturers to propose, construct and certify your card to your requirements and employing their unique processes, techniques and technologies.

One thing you will need to be aware of is how the use of the antenna affects the certification process. It is important to understand that the combination of ink, materials and methods of construct means; each construction will need to go through a unique certification. This need for certification is a result of the use of radio frequency to communicate between the card and the terminal. Think of your cell phone when your inside a big building or within an elevator and how the conversation maybe disrupted. It is this possibility of the radio signal to be disruption based on the materials employed and the method of construction.

When metal elements like metallic foils and layers are used in card construction, the challenge increases. Eddy currents are emitted by the metal and will interfere with the level of power and quality of communications emanated by the antenna and radio in the POS received by the antenna and the computer in the card.

So far we have spoken only of the hardware. The chip in the card is a computer and needs an operating environment, application and data in-order to function. The introduction of the contactless interface alters the operating environment, the payment applications and the data which is loaded into the card. All of this impacts the card manufacturing and card personalization process.

Will the US truly embrace dual interface cards or is our phone the future

When the US decided to migrate to EMV, it took the safe course

When it was time to migrate to EMV here in the USA, both issuers and acquirers focused on addressing the market and the required technology, one step at a time. They recognized the confusion created by the Durbin Amendment, the reality of the competitive US debit market, the complexity of the merchant environment and the legacy infrastructure underneath the American card payment system. Unfortunately unlike in other parts of the world the American merchants tended to migration to EMV in the following order credit & debit, Common AID, contactless (MSD mode), Mobile Pays and finally contactless (EMV mode). This journey is still a long way from complete with less than 25% of the terminal base contactless enabled, let alone in EMV contactless mode.

The larger and most invested merchants also worried about the impact of sharing data with the likes of Amazon, Google and Apple. The “honor all card” rule is also the “honor all wallet” requirement. Wal-Mart, Target and Home Depot were clear, they did not intend to expose the NFC antenna to the various NFC Mobile Wallets. Instead they are implementing solutions, post MCX, based on their mobile apps using QR codes and often times enabled to support frictionless payment.

We are now looking at the second wave of card issuance and Issuers are wondering what merchants will finally do about enabling contactless. As the Issuers prepare to issue their cardholders with their second EMV enabled card they must also think about the future of the card in the context of the future of mobile payments.

Are the payment credentials carried in the mobile wallet the companion of the card

or

Is the card the companion (fallback) for the payment credential carried in mobile wallet / deviceOr

Are we on a journey to a new paradigm

Where facial recognition, loyalty, geolocation

Enabled by the always connected devicesWe surround ourselves with

Help merchants to focus on

the shopping experience

And

Turn the Payment intoA frictionless “thank you”

The case for Identification and Authentication

As we continue to explore the case for Identification and Authentication I share the below article.

What is becoming clear is standards are being embraced.

In the Payment space

Will it be W3C WebAuthN, 3DC and Webpayments or EMVCo SRC & Tokenization?

My guess depends on if standards bodies can play well together. EMV (contact or contactless) will remain the many stay for physical world commerce, until the App takes over the Omni Channel shopping experience. then the merchant will properly authenticate their loyal customer and use card on file scenarios for payments. The question of interchange rates for CNP will see a new rate for “Cardholder Present&Authenticated/ Card Not Present.”. In time when a reader is present I can see an out of band “tap to pay” scenario emerging using WebPayments and WebAuthN.

In the identity space

I contend the government and enterprise market will go for a pure identification solution with the biometric matched, in the cloud, in a large central database. In order to maintain a unique and secure cloud identity, they might probably make use of various opportunities that come their way (you can hover over at this website to learn more).

However, does that mean it includes what you know username, email address or phone number? Maybe! If it is simply the captured image or behavior, then it is a 1 to many match. If it is with an identifier, it is classic authentication with a one-to-one match.

In the pure authentication space where the relying party simply wants to know it is the person they registered. Then, the classic FIDO solutions work perfectly and will be embedded into most of our devices. Additionally, the use of a visitor sign in sheet synced with the security database could expedite the sign-ins of visitors. It could also see its applications with employee log authentication and verification. Or, as we’ve seen with some enterprises, the relying party will embrace U2F with be a FIDO Key, like what Yubico and Google recommend.

The classic process needs to be thought about in respect to what can be monetized.

- Enrollment = I would like to become a client or member

- Proofing = Ok you are who and what you claim, we have checked with many to confirm your Identity – This is where federation comes in.

- Registration – Verification = Ok, now we confirm it is you registering your device(s)

- Authorization & Authentication = Transaction with multiple FIDO enabled relying parties using your duly registered authentication.

How Microsoft 365 Security integrates with the broader security ecosystem-part 1

by toddvanderark on July 17, 2018

Today’s post was coauthored by Debraj Ghosh, Senior Product Marketing Manager, and Diana Kelley, Cybersecurity Field CTO.

This week is the annual Microsoft Inspire conference, where Microsoft directly engages with industry partners. Last year at Inspire, we announced Microsoft 365, providing a solution that enables our partners to help customers drive digital transformation. One of the most important capabilities of Microsoft 365 is securing the modern workplace from the constantly evolving cyberthreat landscape. Microsoft 365 includes information protection, threat protection, identity and access management, and security managementproviding in-depth and holistic security.

Across our Azure, Office 365, and Windows platforms, Microsoft offers a rich set of security tools for the modern workplace. However, the growth and diversity of technological platforms means customers will leverage solutions extending beyond the Microsoft ecosystem of services. While Microsoft 365 Security offers complete coverage for all Microsoft solutions, our customers have asked:

- What is Microsofts strategy for integrating into the broader security community?

- What services does Microsoft offer to help protect assets extending beyond the Microsoft ecosystem?

- Are there real-world examples of Microsoft providing enterprise security for workloads outside of the Microsoft ecosystem and is the integration seamless?

In this series of blogs, well address these topics, beginning with Microsofts strategy for integrating into the broader security ecosystem. Our integration strategy begins with partnerships spanning globally with industry peers, industry alliances, law enforcement, and governments.

Industry peers

Cyberattacks on businesses and governments continue to escalate and our customers must respond more quickly and aggressively to help ensure safety of their data. For many organizations, this means deploying multiple security solutions, which are more effective through seamless information sharing and working jointly as a cohesive solution. To this end, we established the Microsoft Intelligent Security Association. Members of the association work with Microsoft to help ensure solutions have access to more security signals from more sourcesand enhanced from shared threat intelligencehelping customers detect and respond to threats faster.

Figure 1 shows current members of the Microsoft Intelligent Security Association whose solutions complement Microsoft 365 Securitystrengthening the services offered to customers:

Figure 1. Microsoft Intelligent Security Association member organizations.

Industry alliances

Industry alliances are critical for developing guidelines, best practices, and creating a standardization of security requirements. For example, the Fast Identity Online (FIDO) Alliance, helps ensure organizations can provide protection on-premises and in web properties for secure authentication and mobile user credentials. Microsoft is a FIDO board member. Securing identities is a critical part of todays security. FIDO intends to help ensure all who use day-to-day web or on-premises services are provided a standard and exceptional experience for securing their identity.

Microsoft exemplifies a great sign-in experience with Windows Hello, leveraging facial recognition, PIN codes, and fingerprint technologies to power secure authentication for every service and application. FIDO believes the experience is more important than the technology, and Windows Hello is a great experience for everyone as it maintains a secure user sign-in. FIDO is just one example of how Microsoft is taking a leadership position in the security community.

Figure 2 shows FIDOs board member organizations:

Figure 2. FIDO Alliance Board member organizations.

Law enforcement and governments

To help support law enforcement and governments, Microsoft has developed the Digital Crimes Unit (DCU), focused on:

- Tech support fraud

- Online Chile exploitation

- Cloud crime and malware

- Global strategic enforcement

- Nation-state actors

The DCU is an international team of attorneys, investigators, data scientists, engineers, analysts, and business professionals working together to transform the fight against cybercrime. Part of the DCU is the Cyber Defense Operations Center, where Microsoft monitors the global threat landscape, staying vigilant to the latest threats.

Figure 3 shows the DCU operations Center:

Figure 3. Microsoft Cyber Defense Operations Center.

Digging deeper

In part 2 of our series, well showcase Microsoft services that enable customers to protect assets and workloads extending beyond the Microsoft ecosystem. Meanwhile, learn more about the depth and breadth of Microsoft 365 Security and start trials of our advanced solutions, which include:

Something to wonder about

What You Have

The Two Sided Market

When we think of investing in various macro business needs e.g. revenue. We see that establishing relationships with customers to stimulate sales is why we create the goods and services, hopefully, others want.

If the buyer has something the seller wants, in exchange for the good or service they desire, then a transaction occurs. The challenge is simple, each party defines the value of what they are providing or exchanging and presto the trade occurs.

When society grows and the complexity of what each of us produces and when our needs are not aligned to this process called barter, a means of monetization is established. Society creates a trusted form of exchange – pebbles, coins, money, a promissory note or now even cyptocurrencies.

In other words, society creates an answer to enable the exchange of goods and services between parties who do not have goods and services the other party seeks in exchange.

With cash, coins or other trangible representations of value, commerce is easy. When we complicate things and worry about carrying cash and seek to buy things with debt. A need for a Network emerges.

These payment networks, by necessity, add complexity. They create the need to establish two sides to the market, one focused on the relationship with the buyer and the other with the seller.

Issuance and Acceptance. Two words to descibe the two sides of a network. It’s only when the two sides of the market have sufficient participants. Only at the tipping point, enough critical mass exists, to create a self sustaining network. This is the network. At this moment the network blossoms. If either side of the market does not achieve critical mass, the network collapses.

Any two entities familiar and trusting in the Brand, or each other, can easily establish a temporary relationship. Adding anonymity to the requirements, increases the leave of trust and recognition the Brand must establish.

In a digital environment we have to define mechanisms to share and establish trust across trillions of electrons. The two sides will not pursue understanding of nor focus on security. Until the risk exceeds a threshold unique to each party on either side of the market.

To often in the past, the idea of the individuality of the individual or the need to design security in from the beginning. Has left us with a legacy of system all needing design of custom approaches to how to integrate security with requisites necessary to capture, calculate and manage risk.

The Artifact of Trust

When a mutually trusted set of parties gives the citizen, consumer, employee or courtier a card, a device or an object and provides every acceptor with a reader capable of recognizing the trusted thing; then the two parties are in a position to establish “trust”. The consumer has a thing which is recognized and trusted by the acceptor. This is often referred to as “What You Have”.

Once the thing is recognized by the acceptor, then, the process of identification and authorizations (the transaction) can take place. The object – the artifact – carries an identifier. It possesses characteristics that establish its unique character. The object also posesses a means of assuring the acceptor the presentation of that identifier repreents a unique entity.

The simplest artifact of establishing “trust” is a hand held thing, be it a key, fob, card, watch, pendant, phone, ear piece. It does not matter what it is, all that counts is that the merchant recognizes it and that the consumer is willing to carry and present it.

Trust, for the merchant, means they can, according to the rules, recognize and authenticate the thing. They are then in a possition to pursue a temporary and trusted relationship. What can be achieved during the time the relationship of trusted is bounded, is the constrained by an additional layer. In this layer the consumer, the acceptor and any third parties address which the rights and privileges are to be granted or pursued. This is when the exchange, sale, conversation, tranaction, event or access is granted.

Two sides meet several common mediums of exchange are available.

[contact-form][contact-field label=”Name” type=”name” required=”true” /][contact-field label=”Email” type=”email” required=”true” /][contact-field label=”Website” type=”url” /][contact-field label=”Message” type=”textarea” /][/contact-form]

Mobile Payment – Thoughts after listening

Thoughts resulting from The webinar Doug King of the Atlanta Federal Reserve gave on “Future Proofing Payments”

The long standing question of the future of Mobile Payments, again discussed and again similar conclusions.

- Will the American market embrace the idea of mobile payments?

- Is it a question of when or a question of why?

- Why do emerging markets embrace new ways and mature markets resist?

- Is it all about acceptance and the merchants investment in contactless reader capability?

- Is it an all or nothing concern?

- Could it be simply reality, as ling need our wallet with other cards e.g. our drivers license, why eliminate payment cards from the physical wallet?

Doug touched on all of these questions. He shared relevant statistics demonstrating the slow and possibly indistinguishable grow in usage of mobile wallets. He shared the success of several of the merchant proprietary mobile payment approaches.

Which leads me down the path of another question. What is the value proposition that will ignite the use of our phone and devices as carriers of our means of payment? The possibility to create value simply with a electronic wallet carrying only means of payment, does not create an exciting proposition.

Our mobile phones and connected devices provide us with such value

We have embraced dozens of apps. They help us to navigate, shop, explore, play and learn. Our phones are beginning to become security devices, taking advantage of sensors to integrate biometrics into how we access and authenticate ourselves as we browse and explore the ever increasing digital place we now call cyber space.

There is another phenomena emerging as a result of how we are transforming how we engage. Some called it the “Uberization” of payments, the ability to make payments frictionless. A change so profound we must stop and reflect and ponder what next.

I recognize there is a repetitive theme to my musing.

When physical world merchants fully embrace the concept of omni channel and build their virtual and physical experiences to complement and augment one another, then, with the ability to integrate payment seamlessly into the shopping experience a value proposition emerges.

What is EMVCo goal with the release of their SRC framework

October 2017 EMVCo published version 1.o of their Secure Remote Commerce Technical Framework. Today I decided to read and appreciate what they are trying to accomplish and then consider how it ties into what I remember and think we need to do moving forward.

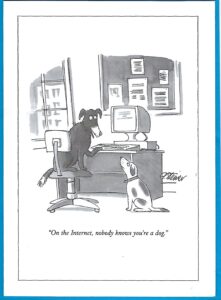

Clearly the challenge links back to the now infamous New Yorker Cartoon.  We have not successfully established a means of assuring the identity of an individual when presenting payment credentials (the PAN, Expiry date, name, billing address and CVV. The first attempt, still not 100% implemented, was the introduction of CVV2, CVC2 or CID a 3 or 4 digit number printed on the back or the front of the payment card.

We have not successfully established a means of assuring the identity of an individual when presenting payment credentials (the PAN, Expiry date, name, billing address and CVV. The first attempt, still not 100% implemented, was the introduction of CVV2, CVC2 or CID a 3 or 4 digit number printed on the back or the front of the payment card.

We then developed something called SET or Secure Electronic Transactions and unfortunately the payment networks were not willing to allow Bill Gates and Microsoft to earn 0.25% of every sale for every transaction secured by SET he proposed to build into Microsoft’s browser. Without easy integration into the consumer browser, the challenges of integrating SET into the merchant web pages and the Issuer authorization systems caused this effort to fail the death of some many other noble but complicated attempts to create a means of digital authentication.

Next came 3D-Secure, a patented solution Visa developed. It offered what was considered a reasonable solution to Cardholder authentication. Unfortunately, given the state of HTML and the voracious use of pop-ups, the incremental friction, led to abandon shopping carts and consumer confusion. Another aborted attempt at Internet fraud mitigation.

Yet 3D-Secure was not a total failure. Many tried to enhance it, exploit it and avail themselves of the shift of liability back to the Issuer. Encouraging consumer engagement and adoption was futile in some markets mandated and cumbersome in others.

Now let’s consider what EMVCo is attempting to do with their Secure Remote Commerce Technical Framework. As I started to read, I ran into this:

“As remote commerce becomes increasingly targeted and susceptible to compromise, it is important to establish common specifications that protect and serve Consumers and merchants.”

Clearly the authors do not have institutional memory and cannot remember the various attempts alumni of these same organizations spent time on and encouraged many to invest in their implementing. Clearly this lack of historic context will leave some pondering the purpose of this paper.

I then read this sentence and reflect back on a recent hearing on “Social Security Numbers Loss and Theft Prevention” in front of The House Ways and Means Subcommittee on Social Security

“Over time the Consumer has been trained to enter Payment Data and related checkout data anywhere, making it easy for bad actors to compromise data and then attempt fraud.”

Once again, I stand troubled by how the Payment Data clearly printed on the face of the card and especially the PAN, 11-19 digits, designed to simply be an identifier, was converted into an authenticator. Like the social security number, the drivers license number, the passport number and your library card number, the PAN and other “Payment Data” was never designed to be an authenticator. It was meant to be data a merchant could freely record.

The secure features of the card now the EMV cryptographic techniques otherwise referred to as the Application Request Cryptogram “ARQC”

now the EMV cryptographic techniques otherwise referred to as the Application Request Cryptogram “ARQC”  were meant to offer the “What You Have” factor in a multi-factor authentication scheme.

were meant to offer the “What You Have” factor in a multi-factor authentication scheme.

As I began to appreciate the scope of this document, the term “Consumer Device” becomes critical. I began to wonder if a PC is a consumer device or if a consumer device is only something like a mobile phone, watch or other like appliance. Fortunately, later in the document, the definition clears up any confusion created by the earlier use of this term.. This said, I then wonder about the difference between what they define as Cardholder Authentication and Consumer Verification?

After reading through all the definitions, I ponder why the authors had to change terminology? Why could they not embrace known and recognized nomenclature. Do we need a new vocabulary?

I wondered:

If this is another attempt to create a revenue stream for the payment networks?

Or, is this the effort of a “closed standards” body to reduce the potential value of the W3C WebPayments activity?

In search of an answer to this last question, I found this discrete comment inside the SRC FAQ.

9. Are any other industry bodies working in this area?

EMV SRC is focused on providing consistency and security for card-based payments within remote payment environments.

EMVCo aims to work closely with industry participants such as W3C to capitalise on opportunities for alignment where appropriate.

Having read bits and pieces of this and the WebPayments efforts one does wonder what is EMVCo trying to do. We shall see?

Why do we need Tokens and Tokenization

Recently I was directed to a link http://paymentsjournal.com/tokens-work-because/ and wanted to write the author Sarah Grotta. As I wrote the message crystallized in my head and maybe as this prior post already discussed, this idea of tokenization made me cringe.

I contend that Tokens exist because we turned the PAN Personal / Primary Account Number, like we turned the SSN Social Security Number, into an authenticator. One can must ask the question. How can a random value (an identifier) become an authenticator and remain secure?

EMV works because it renders the Card unique, hence addressing the question of counterfeit, by employing the first factor of the classic MFA Multi-Factor Authentication concept “What You Have”. EMV defined a common set of secrets and digital credentials; securely stored in a Secure Element or Chip Card.

“What You Have”. EMV defined a common set of secrets and digital credentials; securely stored in a Secure Element or Chip Card.

We here in the United States decided not to implement the second factor, the Personal Identification Number or PIN, for a variety of reasons. Hence, why Lost and Stolen remains an issue or weakness in the American Card Payment environment.

Biometrics are emerging and could solve for the assurance of cardholder presence. The challenge is how to effectively (cost and convenience) locate the biometric sensor and facilitate the matching of the sensors output to the persons registered biometric. Let alone, how does one make sure the right persons biometric was registered and associated with the device.

In the mail order / telephone order, now cyberspace, we did not replicate merchant authentication, the first factor – “What You Have. The card, once was secured with things like the magnetic stripe, using CVV1, the Hologram and the other physical features. We simply shifted the liability to the merchant and called it a “card not present” transaction.

People can claim all sorts of goodness because of tokenization. They can talk about how the EMVCo’s tokenization framework describes the use of tokens in device and domain specific scenarios. All of this, an issuer, could have done; if they, like some did, simply issued another number, a PAN, to the wife, bracelet, watch, ring or whatever other permutation they deemed appropriate. They can talk about dynamic data. yet what they often forget to include when they use the words “Dynamic Data” they are really talking about a cryptographic value as described in EMVCo Book 2.

Yes, this does mean the question of how the PAN and its digital credentials get deployed; has to be addressed. This said, GSMA with EPC did offer some thoughts, last decade, when they described the Trusted Service Manager

Instead handset oligopolies replaced the MNO with the their Mobile Pay wallets. They working with the ![]()

![]() Payment Networks and focused on control and the creation of income. They, as monopolist will, have created barriers, restricting others from offering comparable services. The TSP now becomes this restrictive service that guarantees the power of companies like

Payment Networks and focused on control and the creation of income. They, as monopolist will, have created barriers, restricting others from offering comparable services. The TSP now becomes this restrictive service that guarantees the power of companies like

Apple and Google, supported by their friends, the payment network operators.

Apple and Google, supported by their friends, the payment network operators.

The original article also spoke of the PAR; another data element merchants, processors and the industry, will have to invest in supporting.

I ask the question.

If we had assured the authentication and verification of every payment transaction

Using Multi-Factor Authentication

Why did we need to turn the PAN into a dynamic value?

My contention, simply use the appropriate level of cryptography.

If the Issuer or their processor is in control and understands basic EMV and Cryptography, then securing the PAN is not an issue.

If the Issuer or their processor is in control and understands basic EMV and Cryptography, then securing the PAN is not an issue.

Consider household financial management. If each member of a household has a unique PAN; budget, tax preparation and understanding who spent what where is a lot easier. The husband,wife and children should have their own unique PAN, stored in the clear in their devices and on their card.

The real requirement, my personal devices, including my payment card, simply need to be linked to one PAN their Personal Account Number, associated with the individual. The PAN Sequence number could easily allows each device to be uniquely identified, if necessary. The card and devices becomes the carrier of your identifier. A thing that can be authentication as something you have.

Here is where the second factor comes in. Is the person presenting the PAN the rightful and authorized individual? All this required, is assurance to the shareholders that the presentment of the PAN is a unique and authorized event. This is best achieve by using either something you know or something you are to bind the individual to the instrument carrying the Identifier.

Yes, a bit of friction to assure the consumer they are securely paying for what they want to buy

Since the World Wide Web came of age and merchants saw its potential. The question of how to secure the  Card Not Present space, this question of cardholder presence, has not been properly addressed. Visa and MasterCard (when they were not for profit associations) created the utility of the Card Verification Result CVV2, CID or CVC2 which would be printed on on the card and not part of the magnetic stripe, the problem the bad guys could still steal the card or get hte card number and capture CVV2.. MasterCard and Visa then created SET, 3D-Secure and now, as for profit owners of EMVCo, are proposing, maybe even will mandate, the industry implement EMV 3D-Secure.

Card Not Present space, this question of cardholder presence, has not been properly addressed. Visa and MasterCard (when they were not for profit associations) created the utility of the Card Verification Result CVV2, CID or CVC2 which would be printed on on the card and not part of the magnetic stripe, the problem the bad guys could still steal the card or get hte card number and capture CVV2.. MasterCard and Visa then created SET, 3D-Secure and now, as for profit owners of EMVCo, are proposing, maybe even will mandate, the industry implement EMV 3D-Secure.

Each, an attempt to provide some means of Authentication and Verification.

Each introducing a level of friction as a means of security.

This is the problem. The market did not start by emphasizing the need for security by educating the consumer. The industry needed to help the consumer understand they should care and want to securely pay for what they intend to buy.

Instead:

- The Zero Liability Policy was adopted.

- The merchant was more than happy to sustain a degree of lose (fraud) in exchange for sales and profits.

The result, as all anticipated would happen, was blissfully ignored and eventually they cried out about.

Fraud migrated to the weakest point

Just like water finds its way to the lowest point.

EMV, introduced in the Face to Face card present environment, pushing the bad guys: be they criminals, state actors and terrorists to find alternate another channels for their financial gain.

be they criminals, state actors and terrorists to find alternate another channels for their financial gain.

EMV and now the recently published WebAuthN and FIDO specifications create effective mechanisms for Consumer Authentication.

Let us please remember – the PAN, a user name, your social security number or your email address are excellent Identifiers. They should not be authenticators and they are not a means of “Identification”.

Let us also remember, the term Identification means that one is assured of the irrefutability of identity.

The big question:

- Why did we have to get rid of or replace the PAN?

- Why did we and continue to need to invent and invest in all this addition overhead?

- Why did we not simply address authentication?

Some will argue the challenge of using the PIN or a Password, as a means of Verification, is because it is to hard to remember. Especially, if each password people use to access website, services, building, has to be unique. Some will argue imposing friction to add security is not convenient. Others will remind us that security is and has been a necessity since the beginning of time.

Why didn’t we when we created this great new digital shopping mall?

Bottom line each of the devices used to present or acquire the PAN, must be capable of authenticating the identity of the authorized presenter, in both the physical and virtual world.

At least these are the views of someone who believe history provides a baseline for tomorrow and tomorrow must be designed as a function of where you want to be, knowing where things came from.

Of NFC, Mobile and History

Today I read Karen Augustine’s Mobile Payments Use in the U.S. Lags

As I read and reflected on what Karen wrote, I reflected on my experiences as a sagged payment consultant and executive, with international experience.

What I see is an issue of legacy and muscle memory – setting a pattern for the future. Said another way – our history defines the boundaries of our future.

Asia did not have electronic payments. I am sure did not want to embrace the globally dominate American solution. Therefore, they had the opportunity to start fresh. It is very much like what Spain went through, went they moved from cash to electronic card-based payments. They bypassed the check.

Her article brings back memories of life in Belgium in the 90’s. Writing a check was a rare occurrence. Direct debit mandates, a MisterCash card

![]() and a Eurocard was all we needed to buy and enjoy life. Electronic payments was the norm, paper checks were a rare oddity and cash, well yes there was a very present grey economy.

and a Eurocard was all we needed to buy and enjoy life. Electronic payments was the norm, paper checks were a rare oddity and cash, well yes there was a very present grey economy.

Here in the USA we developed our payment systems off the back of regional or state banks with acceptance networks limited to a local domain. Moving to a national system required early adoption of a common national currency. We then went on to replace IOUs with paper checks and store cards with credit cards. In time we enhances the ACH system and developed support for remote deposit and check capture.

Why do we need to move the card into the wallet? Why change habits that are comfortable and work? Most of us drive to shop and therefore must have our drivers license. We must carry a physical document with us. We simply carry two or more ID-1 sized cards.

You make the statement and was once again reminded of times past.

“… universal mobile wallets and more often driven from merchant based applications that often incorporate loyalty and rewards, which to date still remain nascent in universal mobile wallets.”

When I produced this rendering, back in 1996, I was on stage talking about a world where leather and technology converged. I imaged Bluetooth, NFC, secure elements, GPS and our various credentials converging into this personal device. Those credentials grouped into: travel, identity, membership, loyalty and payments; easy to find and present.

When I produced this rendering, back in 1996, I was on stage talking about a world where leather and technology converged. I imaged Bluetooth, NFC, secure elements, GPS and our various credentials converging into this personal device. Those credentials grouped into: travel, identity, membership, loyalty and payments; easy to find and present.

When contactless payments were introduced, in 2004, by Visa’s with PayWave and MasterCard’s PayPass; I argued why contactless cards – how can the issuer afford the extra dollar per card (cost of the antenna and inlay) and the merchant the extra 60 dollars to enable the NFC reader? The way Issuer income works, “Interchange”, the consumer would need to spend more on that issuer’s card. For the merchant to justify the necessary POS investment, meant the retailer believed the consumers would spend more, because it was “easier”. Was Tap To Pay going to make me spend more. Maybe for small ticket purchases, I may use cash less; but at the merchants expense! We argued the cost of cash was more than the Merchant Discount. Some agreed. Many wondered what the blank are they trying to sell us!

Around the same time America was exploring this contactless experience, the European Payment Council and GSMA debated and ultimately offered an approach for mobile card based contactless payments https://www.europeanpaymentscouncil.eu/sites/default/files/KB/files/EPC220-08-EPC-GSMA-TSM-WP-V1.pdf . Handset manufactures like Nokia had already added NFC Antenna’s to their mobile phones and mobile network operators, the MNO, saw the SIM as the secure element capable of holding payment credentials.

Some tried, the Trusted Service Manager as a service was developed and deployed. The challenge, the economics of the model. In this case the MNO saw revenue and wanted to charge fees to load the payment credential into the phone and better yet charge rent to store these payment cards in our phones. Again I ask the question, by changing the way we pay, do I cause us to want to spend more? I think not!

Maybe some would argue, with a credit card people am able to buy things today that they cannot afford. Let them end up in debt. This is true. But then is debt at 18% a good thing? Europeans simply decided to establish a line of credit, as a feature of a Current Account, at reasonable interest rates.

We could go on and talk about how Apple saw the possibility of a 0.15% income stream from ApplePay based mobile payments and how the EMVCo tokenization framework evolved to support their desire to protect the Apple Brand.

We could go on and talk about how Apple saw the possibility of a 0.15% income stream from ApplePay based mobile payments and how the EMVCo tokenization framework evolved to support their desire to protect the Apple Brand.

What is clear, we could solve George’s problem and replace his Full Grain Vegetable Tanned Cow Leather leather wallet with a Mobile Wallet managed by Apple, Google, Samsung or …

Or, we could think about the consumer and what they really want?

As your article made clear, and so many others have shared, Asia leaped forward. Be it AliPay or WeChat, the device, the mobile phone, became the consumers wallet, their method of engaging, shopping, learning and exploring.

We need to accept to simply replace what we are comfortable with, with something new; which does not enhance our experience, is simply not worth it!

Many of us, like Karen, would argue the experience of shopping is what the mobile phone can enhance and let the act of payment become the afterthought. A simple click to say – yes, I agree to pay.

Amazon got it right with One Click. Others, as the patent expires, are embracing the same technique to simplify payment to a friction-less act of satisfaction. When my favorite stores offer me an mobile app designed to enhance my shopping experience, to thrill me with offers and entice me with things I want; then yes I will become more loyal, I will shop at their store more frequently and maybe even buy a few things I did not intend to buy.

Many years ago while attending conference of groceries in Abu Dhabi – one of the speakers share an experience. when that supermarket executive instructed each store to put the beer across from the diapers, the intended result occurred. The husband, sent to get the diapers, ended up buying a six pack too.

Maybe, like this experience reveals, if we focus on the consumer experience and on delighting them. They will embrace change.

If there is no value why should we?

Years ago I prepared and published an idea. I called it Cando. I was still committed to the idea of the mobile wallet. I was an early adopter of the smart phone and saw its potential.

Payment Card Construct and Dual Interface Deployment

Payment Card Construction

The discussion focused on the construction of the sandwich. Four layers. Clear front laminate to protect the ink, front with the banks design and brand logo, back with the banks back design and a clear laminate with the magnetic stripe integrated into it.

To enhance design additional layers may be added, such a metal foil.

These four sheets are then bonded together, at 120 degrees, in sheets of 21, 36 or 48 or other various sheet sizes. Next step punch out cards, add hologram and signature panel.

For a standard EMV card the next phase is to mill and embed the module with the chip inside. Last, the manufacturer typically loads the O/S & EMV application into the integrated circuit card.

When we move to dual interface caed, this process is modified to add an inlay, with the antenna embedded within. This inlay is inserted in the middle of the sandwich and during the embedded process the contacts exposed on the base of the module are connected to the antenna in the inlay.

Next step, personalization, when the appropriate data is loaded into the chip, along with the encoding of the magnetic strip and printing and/or embossing of the cardholders, name, expiry date, cvv2 and other information onto the card.

Contactless or Not That is a Question

Contactless NFC acceptance and dual interface issuance is all about the chicken and the egg. Who will go first? The merchant or the issuer? Each need each other. Both are wondering about the incremental value.

- Faster transactions – Yes

- Less cash – maybe

- More revenue – good question!

In other parts of the world, transit and their choice of contactless, as the right answer to a more efficient fare collection solution is driving conversion. In other, markets a group decision to adopt or a desire to find the next great thing drives the market. Here in the USA, we have a less than successful history of contactless. Let’s not forget PayPass and PayWave, it was tried the middle of the last decade, to little or no success.

We have Google and the FinTech world looking to mobile payments as the next great adventure. Merchants, like Wal-Mart, are resisting NFC acceptance given their own plans for QR based wallets and desire to limit the sharing of data with competitors.

Given these questions and observations, one can only wonder.

Financial Trade Groups Write to House Leaders in Support of Data Breach Notification Bill

https://bankingjournal.aba.com/2018/02/financial-trade-groups-write-to-house-leaders-in-support-of-data-breach-notification-bill/

The American Bankers Association and six other financial trade organizations wrote to House leaders today underscoring the need for businesses across all industries to be held to the same data protection and breach notification standards currently adhered to by regulated financial institutions.

The associations expressed support for draft legislation released by Reps. Blaine Luetkemeyer (R-Mo.) and Carolyn Maloney (D-N.Y.) that would create a level playing field of nationally consistent data protection standards and post-breach notification requirements. This bill would not create duplicative standards for financial institutions which are already subject to robust standards, but rather extend similar expectations to other sectors that handle consumer data.

“The goal of the bill is simple — raise the bar so that all companies protect data similar to how banks and credit unions protect their data, and create a common-sense standard to ensure consumers receive timely notice when a breach does occur,” the groups wrote.

The draft bill contains a provision that recognizes the existing, effective regulatory framework for covered financial sector entities. While the provision was intended to prevent banks and credit unions from being subject to duplicative notification requirements, it has been the target of recent negative campaigns circulated by the National Retail Federation and the Retail Industry Leaders Association, which incorrectly suggested that banks do not notify customers of breaches on their computer systems and The ads from the retailer groups also mischaracterize and exaggerate the share of data breaches occurring at banks and credit unions while omitting their members’ (higher) share of data breaches.

The financial trades refuted the notification assertion, noting that “banks and credit unions have long been subject to rigorous data protection and breach notification practices for financial institutions to follow,” and that in the event of a data breach, banks and credit unions work continuously to communicate with customers, reissue cards and enact measures to mitigate the effects of fraud. They added, however, that “no solution will work unless everyone has an obligation to take these steps.” For more information, contact ABA’s Jess Sharp.

Words all bound to who we claim to be – How do we identify ourselves on the Internet or in Cyberspace?

Identifier – Something you create or are provided to digitally identify yourselves. Identifiers are things like an alias, user name, email address are examples.

Identity – This is who we are or wish to represent ourselves to be. These are attributes and information about: where we live, who we work for, which banks we have relationships with, who our friends are, which clubs we belong to, our certified skills, what schools we graduated from, which country(s) we are citizens of, our LinkedIn profile, Our Twitter handle, our Facebook identifier, our phone number … . It is the sum of the attributes we can and will share with others, be they individuals, governments, entities or organizations; as we establish relationships and prove to them who and often what we are.

Authentication – The method we employ to assure that you, based on the identifier presented, are who we (the relying parties) thinks you are. You are the person the relying party accepted when you registered that Identifier as how you would digitally identify yourself. By itself the method of authentication should not allow another party to be able to determine anything about your identity. Privacy is the goal. FIDO Alliance and W3C have defined standards to support authentication.

Verification – The process of confirming that the secret or biometric match the secret or biometric that where originally registered to that Identifier.

Identification – A means of authentication that is bound to your identity. A EMV payment instrument “Chip and PIN”, a PIV card, an electronic passport, a membership card, a drivers license, a national ID are all forms of identification issued by a party that should be trusted to have performed a proof of the individuals Identity, based on a defined and often published criteria.

This particular word, for many, has an alternate meaning. In the biometric community they see Identification as the ability to use a biometric to determine ones Identity. This is achieved by performing a one (the person present) to many match (persons registered). The goal is the same, bind Identity to the mean of Authentication by using the Biometric as the Identifier.

Proof – The method a relying party or an individual uses to validate your claim of a specific Identity. In many cases this is achieved by relying on knowledge of another party. The relying party accepts the due diligence to proof your claimed identity was done to their satisfaction by another party. This other party is often referred to as a Trusted party. This effort to proof the identity of an individual is linked to words and acronyms like KYC “Know Your Customer”, ID&V “Identity and Verification” and Self Sovereign Identity. We classically assume that documents provided by a Government e.g. drivers License and Passports are a solid proof of the claims asserted on those same documents.

In a digital world this is the most important element of a how we as people, entities, governments and corporations can be assured that you are who we believe you to be.

I am once again am reminded of the 1994 New Yorker Cartoon

Europe Led the way with EMV yet Europe appears to prefer cash

Europeans still love paying cash even if they don’t know it

Interesting to reflect on how much we allow Europe to lead as we think about EMV and the technology we use to secure our payment cards. Maybe American’s need to embrace and take over the management of these key standards that drive an economy.

Thinking about cards

In 1991 I had to learn the difference between million dollar transactions and hundred dollar transactions. As I came to explain, when telling my life story, I had to shift my thinking from 100 transactions at a million to 1,000,000 for a hundred. This transition took me from capital markets to payment cards.

Today, I wonder about the future of the ID-1 based payment card? A piece of plastic 3 3/8 x 2 1/8 with rounded corners.

In another blog I spoke of how this ID-1 object became a token responsible to act as the first factor, something you have. Printed, encoded and embossed characteristics were the security features. Today, with EMV as the global standard for payment CARD security; cryptography and the “secure element” replace those physical security with digitally mastered circuitry embedded inside something capable of protecting those secrets cryptography requires. We digitized the payment card. What we now must do is shift our vocabulary to tokens and credentials.

We need to embrace a new way of speaking we need to think about our “Payment Credentials”.

Today, we now tap our phone to pay, we use our phone to browse the internet, we shop & book tickets with apps and we listen to music & watch movies all from this device we apparently use, thousands of times a day. For those of us who remember computers that filled floors, we now are capable of buying more powerful computers, similar in size to those same cards. Think about the Raspberry Pi, a computer almost as small as a card, not quite! Yet!

The embedded secure element integrated inside our payment cards are being integrated into phones, bracelets, rings and things. The question; will they replace the card we are now comfortable with? Yes – maybe? Will we embrace these objects as the new carriers of our payment credentials? Many hope so.

In oder to think about the probability of cards disappearing, one must begin by think about the number of cards now in circulation. In round numbers we can think about 1.2 billion debit and credit cards, 300 million prepaid cards and 300 million retail branded cards. In round numbers, 1.8 billion payment cards. We next must think about our population and how many people now carry cards – 115 million households and 242 million Americans over the age of 16, according to a recent census. We now has a numerator and a set of denominators.

The question then becomes, how many payment cards does an American want to carry and how many payment credentials will an American end up having.

I would argue a debit card and a credit card is all we need to carry in our leather wallet, purse or pockets. Those other payment credentials can easily be accessed from wallets in the cloud or in our digital objects.

Merchants can integrate payment capabilities and focus on factoring their consumer receivables, behind relationships designed to service, thrill and sell. In an App and API enables economy, cards become a burden as the experience becomes the essential component of our lives.