As a member of a committee responsible to develop the agenda for Payment Summit this February in St Lake City, we’ve been discussing a panel on Cryptocurrency. The initial conversation spoke of blockchain and cryptocurrencies and how these two topics, while related, need to be independent of each other.

With an agreement to focus on Cryptocurrency, I began to ask myself, “What is a cryptocurrency”?

Off to the Internet. My computer instantly offered a definition.

A digital currency in which encryption techniques are used to regulate the generation of units of currency and verify the transfer of funds, operating independently of a central bank

-

-

-

- ‘decentralized cryptocurrencies such as bitcoin now provide an outlet for personal wealth that is beyond restriction and confiscation.’

- ‘States will undoubtedly resist the spread of cryptocurrencies.’

- ‘Bitcoin was the first widely used cryptocurrency, but few people know it is not the only one.’

- ‘What does your cryptocurrency allow people to do that they could not do otherwise, and how does it help them do existing tasks more quickly or cheaply?’

- ‘If cryptocurrencies are like other speculative activities, the early players and the big players benefit to the detriment of the late entrants and the small players.’

- ‘As with all cryptocurrencies, price is based on supply and demand.’‘Even with recent fluctuations, the total value of the cryptocurrency is still over eight billion USD.’

- ‘The majority of cryptocurrency activity still appears to be speculative.’

- ‘A cryptocurrency may be hackable, but it can also be really, really, really hard to hack—harder than robbing a bank.’

-

-

The interesting challenge in this definition is the words “operating independently of a central bank”.

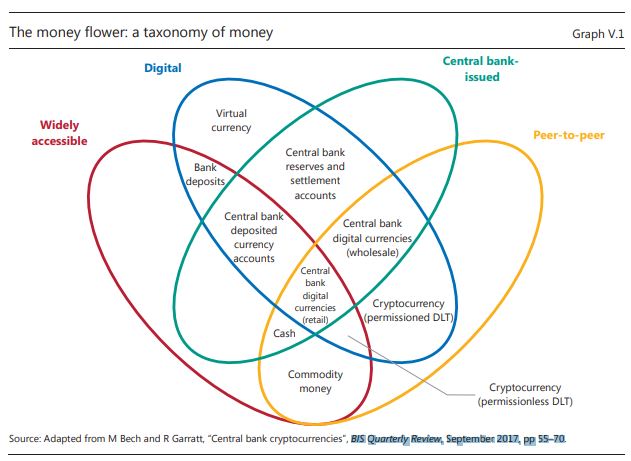

In September 2017 the Bank of International Settlement BIS published a report on Cryptocurrencies. This report spoke to the idea of CBCC or Central Bank Cryptocurrency. The authors offered a diagram known as the Money Flower. The flower positions this idea of CBCC within the world of money and argues a Central Bank could easily create a sovereign cryptocurrency.

The article then goes on to describe a series of examples. As I moved through the document I was drawn to the idea of Digital Currency and once again was compelled to search for clarity. At the same time I noted the recent announcement by China and how the European Union recently suggested the European Central Bank consider just such an investment.

During my research, I was reminded of the work of David Chaum and remembered how early in the growth of Bitcoin someone suggested David could be Satoshi Nakamoto. I am also reminded of my time at Europay and how we explored the use of Chip Cards, given their hardware and cryptographic capabilities, to create a Cash Replacement, Mondex. In parallel with our efforts Visa Cash emerged, Proton, Chip Knip, Chipper and, others emerged. This led me to a BIS report on Electronic Money.

Looking back in history to the early discussions of Electronic Money and read the early views of the European Union and the US Treasury, it reminded me of some of the original concepts and issues. I’m reminded of words like anonymity, traceability, origination, and sovereignty.

Anonymity and the lack of traceability are what criminals and Silk Road Market Place saw as the benefit of Bitcoin. The concepts of origination and sovereignty clearly are key to the thinking of Governments and Central Bankers and critical elements of the origin of Bitcoin, as expressed in the original white paper.

What these cryptographers have created is amazing, yet one worries about who is responsible for and benefits from the origination of Bitcoins, forks of Bitcoins and the multiple cryptocurrencies now in existence.

If we look inside Bitcoin its architecture promotes the idea of mining and allows the successful miner to originate new bitcoins. They argue this is the incentive driving participation. I then wonder about the cost of Bitcoin mining or the cost of Ethereum mining. Does the cost of supporting Bitcoin justify its continued existence? Does the supposed benefit of cryptocurrencies justify the profit earned by the miners who support the work to assure consensus?

As my research progressed I ran into a speech given at a conference and the Bundesbank Money in the digital age: what role for central banks? The article attempts to address three questions:

-

-

- What is money?

- What constitutes good money, and where do cryptocurrencies fit in?

- And, finally, what role should central banks play?

-

The author’s arguments are worthy of consideration. Especially the questions of efficiency and trust.

The question we all must consider

What is money?

Especially in the global and emerging digital market place.

In the end, I remain confused and concerned. Digital Money, Electronic Money, Digital Currencies, Cryptocurrencies, Feit Money, stablecoins and the potential of the distributed ledger clearly are set to disrupt much.

will ultimately respond to the changes now taking place to how we Log-in to a website. Yesterday, or better said 10 years ago, we all understood that simple User Name password. A single screen with a reasonably consistent user interface. Sometime we might have to put up with two screens, One for the User name and the next for the password.

will ultimately respond to the changes now taking place to how we Log-in to a website. Yesterday, or better said 10 years ago, we all understood that simple User Name password. A single screen with a reasonably consistent user interface. Sometime we might have to put up with two screens, One for the User name and the next for the password.