These cards and often times the terminals are more expensive than a classic “Dip” EMV card

How much, is dependent on volume, complexity and the pure skill of negotiation. This incremental expense is the first factor one must quantify when building the business case

- for enabling, in the case of the terminal

- adding in the case of the card, the contactless antenna

- upgrading the software by adding the contactless terminal kernels or selecting the appropriate chip software and profile

This then must be compared to the incremental value

For the merchant, issuer and ultimately the cardholder

To explore the benefits lets think about

- The user experience

- Availability of merchant contactless acceptance

- The intersect of the cardholder base with the contactless acceptance infrastructure

As we look around the world and consider what stimulates dual interface card issuance and merchant NFC enablement. Two scenarios emerge.

- A country made a collective decision and drove NFC terminal enablement and dual card issua.

- A merchant segment, typically transit, decided to introduce electronic fare-collection.

The first scenario is often driven:

- By the payment schemes

- The belief NFC “Near Field Communications” mobile payments will happen

- A country simply wants to start dual interface and prepare for mobile payments

Which ever option they select, the merchant and financial institutions, within the country, typically migrate together.

In the case of the second scenario, merchant driven migration. We can look to the United Kingdom as a perfect example. “Transit For London” made the decision to migrate from paper tickets to an electronic fare-collection solution based on NFC. The initial deployment was a closed loop payment card, branded the Oyster Card, they quickly decided to upgrade the solution to support Open Loop e.g. Visa, MasterCard and American Express enable dual interface cards and NFC enabled mobile phones.

Given the importance of public transit to the urban demographic. Their decision to embrace open contactless fear collect, becomes a driving factor for issuers and therefore a ripple effect on merchant enablement.

America, as is true in many things, is different.

Contactless was tried last decade without much success.

Issuers did not see any significant lift in consumer spend nor did the merchant see any real increase in revenues. This experiment did not create a perception of a real benefit for either the merchant of the cardholder. Later in this same period, Starbucks launched their QR code mobile payment solution. From its original deployment to now it has been a resounding success.

Around the same time and based on the work of GSMA and the European Payment Council, major telecom operators began toying with NFC based mobile payments. Here in the United States two pilots emerged, the original Google Pay pilot and ISIS (SoftCard) offer. The results were intriguing, the commitment half hearted and frankly both solutions had issues. Google Pay tried to model its solution after de-coupled debit. Whereas the mobile network operators behind SoftCard, wanted to charge the issuers rent and load fees associated with the payment credentials they would store within the SIM.

Merchants Attempted to Create a new Payment Scheme

Major retailers in their continued quest to improve the customer experience and reduce the cost of payments; came together to create MCX the Merchant Commerce eXchange. The hope, merge their existing private label charge card programs together into a Mobile App capable of working across the family of MCX merchants.

Terms where written, in particular one agreeing these merchants would not accept another competing Mobile Wallet. Net result, the merchants agreed not to enable the NFC interface for any of the Visa, MasterCard, Discover or American Express contactless cards or NFC enabled mobile payment devices.

MCX slowly faded into oblivion, as the merchants struggles with the idea of sharing customer relationships and transaction data. Some merchants notably Walmart, Target, Macy’s and Kohl’s set out to build their won mobile wallets embracing QR codes and other none NFC based techniques.

The Introduction of HCE

While this was going on, north of the American border, the idea of HCE “Host Card Emulation” was created by the founders of Simply tapping 2011. It was ultimately by Android and released as part of KitKat in version 4.4 of the Android operating system. With HCE now inside the Android Operating System it unlocked the NFC interface from dependence on the SIM and MNOs. Now any application could take advantage of the NFC interface, once supported by the internarional payments schemes, enabling wider deployment of NFC enabled mobile payments. Google moved ahead to expand its payment ecosystem and Royal Bank of Canada embraced HCE. As Issuers enabled the ability to authorize the load of EMV secured Payment Credentials into the OEM Mobile Wallet or the Issuer’s own mobile app. Consumer now had the opportunity to experiment with mobile payments that communicate with the POS, just like a dual interface card.

Let’s not forget Apple Pay.

Given their brand value and total control of the Apple operating environment, Apple was able to turn to Issuers and suggest they enable the load of EMV secured Payment Credentials into the Apple Pay Wallet. They came at payments with all guns loaded. They knew the value of their brand and were able, unlike the MNOs to ask for a 0.15% of the issuers’ interchange revenue. Most importantly, they facilitated Visa and Mastercard domination of the role of the Trusted Service Manager TSM-SP or better said the Token Service Provider TSP.

Merchant Acceptance Is Key

As has been true with any solution designed to serve a two sided market, issuance and acceptance must grow together to assure the operator success and prosperity. Without a national imperative and with the experience of the original ZIP (Discover), Express Pay (Amex), PayPass (MasterCard) and PayWave (Visa), the merchant must determine if it is worth the effort to enable the NFC interface and train their staff to support Contactless payments.

Transit, like has been true around the world, absolutely sees the value of using contactless, for fare collection and are busy engaging with Visa and MasterCard to embrace and assure acceptance of bank branded dual interfaces cards. Urban areas such as Chicago (CTA), Salt Lake City (UTA), LA Metro, Portland OR (Trimet) and Philadelphia (SEPTA) are live with deployments. Others are in various stages of planned, including the MTA in New York City.

The Business Case

For issuers, where transit is seeking to exploit open loop contactless payments, at the turnstile, there is a revenue opportunity to deploy dual interface cards.

In rural areas or urban communities where public transportation does not exist. The business case is dependent on what local merchants do and if they intend to or will be forced to enable the NFC capabilities of their POS.

This is the big question. Does the merchant see value? Do they believe contactless will increase revenue, reduce time at checkout or do they believe Apple Pay, Android Pay and the other mobile NFC enabled devices are the future?

- If the answer to these questions is yes then Issuers should seriously consider deploying dual interface cards.

- If the jury is still out then the investment in dual interface cards may not yet be worth it!

What is the Future Payment Credential Carrier

One cannot discuss contactless payments without thinking about how Apple Pay, Android Pay, Samsung Pay, OEM Pay, Issuer Pay … Device Pay play into the future of cards. Some years ago there were three belief systems

- Cards are here to stay the mobile device is a fad

- The wallet is replaced by the mobile device

- The card is the token of last resort

I think we know mobile devices are not a fad. Until mobile devices never run out of power they will not replace the wallet or all of the cards.

To say much more, given the fogginess my crystal ball, would be to wild a bet.

The following articles produced by the Secure Technology Alliance offer a series of perspectives on the value of migrating to a dual interface card.

Alliance Activities : Publications : Contactless Smart Cards

Alliance Activities : Publications : Payments : Contactless Payments

Alliance Activities : Events : Webinar: Contactless EMV Payments: Issuer Opportunities

Alliance Activities : Events : Webinar: Contactless EMV Payments: Merchant Opportunities

. How we restore privacy and what will happen as the new GDPR regulations go into force in Europe, and as California moves to introduce its privacy legislation; requires each of us to watch carefully and be part of the move to restore the consumers’, OUR, right to the data that is us.

. How we restore privacy and what will happen as the new GDPR regulations go into force in Europe, and as California moves to introduce its privacy legislation; requires each of us to watch carefully and be part of the move to restore the consumers’, OUR, right to the data that is us.

As these loses escalated, the cost of the various techniques to support more secure authentication have been developed. The market always understood if we could merge a unique object something you Have, with a secret you Know or a biometric something you Are; you would be able to establish a superb form of multi-factor authentication. Many, such as the ICAO, EMV and PIV specifications, embraced the idea of cryptography operating within a secure element or smart card. They further embraced the idea of loading the registered biometric rending into the chip and incorporate the matching algorithm within the software. By then using an external PIN pad or biometric sensor, multi-factor authentication could be enabled. Unfortunately, at considerable cost.

As these loses escalated, the cost of the various techniques to support more secure authentication have been developed. The market always understood if we could merge a unique object something you Have, with a secret you Know or a biometric something you Are; you would be able to establish a superb form of multi-factor authentication. Many, such as the ICAO, EMV and PIV specifications, embraced the idea of cryptography operating within a secure element or smart card. They further embraced the idea of loading the registered biometric rending into the chip and incorporate the matching algorithm within the software. By then using an external PIN pad or biometric sensor, multi-factor authentication could be enabled. Unfortunately, at considerable cost. displaying a onetime password as the answer. In some cases, the user had to first enter a PIN then a number displayed on the screen and then type the value displayed on the device into a field in browser window.

displaying a onetime password as the answer. In some cases, the user had to first enter a PIN then a number displayed on the screen and then type the value displayed on the device into a field in browser window. Something you have with a secret, a one-time password, unique to each event.

Something you have with a secret, a one-time password, unique to each event.

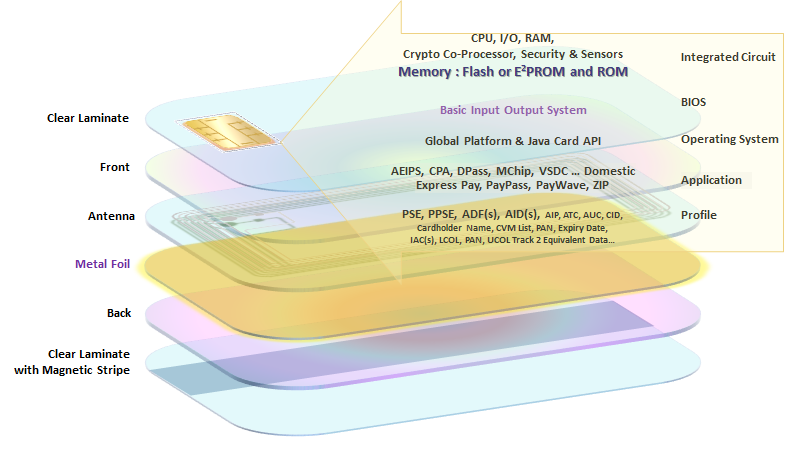

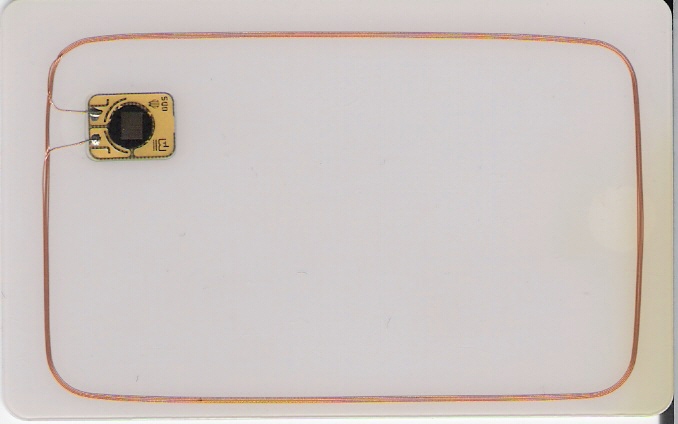

When we think about the migration to contactless or Dual Interface cards it is important to have a general understanding of what goes into creating the card and the constraints one has to think about, as they work with their marketing teams to design these cards.

When we think about the migration to contactless or Dual Interface cards it is important to have a general understanding of what goes into creating the card and the constraints one has to think about, as they work with their marketing teams to design these cards.