This morning I read an article in the Financial Times The real story behind push payments fraud. What is disturbing, the acceptance of fraud and the focus of bankers on adding fees (like Interchange) to help cover the cost of fraud. This article speaks to Push Payments and how liability shifts from the merchant back to the Issuer and ultimately the consumer. It makes reference to Pull Payments and the use of debit cards where the fraud liability, unless online, is the merchants’.

To address card payment fraud in the physical world the payment schemes developed EMV. In the digital or eCommerce realm everyone accepted allowing the merchants to not attempt to authenticate the cardholder and simply ask the consumer to provide openly available data {cardholder name, PAN the account number, expiry date, and address details}; if they, the merchant, would accept liability for any fraud.

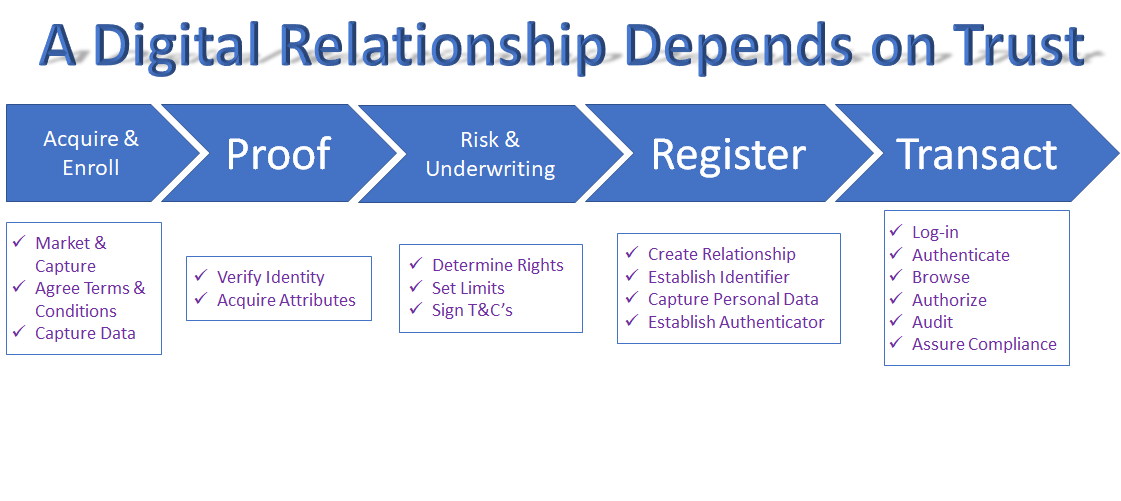

As the world moves to embrace “Faster Payments” and Real-Time Gross Settlement ‘RTGS’, instead of focusing on assuring the identity of the sender and the recipient; we assume fraud will occur.

Why not focus on solving the problem? Solving for Digital Identity solves for Card Not Present fraud, RTGS fraud, Faster Payment fraud, and so much more.