II ePayments - The Enabler for eCommerce

Assuming identity can be guaranteed, deciding which payment

system to make available on the Internet is the next most important issue

holding back the growth of eCommerce. Obviously, paper notes and coins will not

work. The system must be electronic. Most people are already aware of

electronic payment systems such as American Express, Diners, JCB, MasterCard,

and Visa, and can rightly ask, "Why should we use anything else?"

Security is an essential attribute of these networks. They have been introduced

and accepted by buyers and sellers worldwide. Rather than inventing something

completely new, these existing systems offer an obvious starting point for an

ePayment system[1].

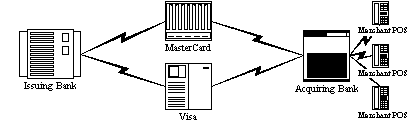

EFTPOS - The Virtual

Private Network

The bank payment associations such as Visa, MasterCard and

Europay have built a secure global network designed to carry authorization,

clearing and settlement data. These are all Virtual Private Networks. Core to

their design is an assurance of security necessary to protect sensitive payment

details while guaranteeing that no transactions are lost. Other networks, such

as those managed by S.W.I.F.T. and the ACH operators have a similarly

construction. All have well-defined messaging standards, comprehensive

operating procedures, and certification processes to assure security and

reliability.

The Internet - A Public

Utility

In contrast to the VPNs, the Internet has evolved as a

public utility with no inherent security or guarantee that transactions are

complete. Its power is to allow any

buyer to find a seller anywhere on the globe. Organizations see the Internet as

an extremely powerful distribution channel without the cost of building and managing

a physical storefront or the expense of running a global mail order and

telephone order operation.

Consumer Fear - The Brake to Exponential Growth

Media publicity about the ever-present reality of fraud over

the Internet has created suspicion and distrust in the minds of buyers about

entering their personal or their company credit card details onto the Internet.

The fear of fraud is real; particularly when one considers the open

architecture of the Internet and the ease this offers hackers and criminals to

intercept credit card data transiting the Internet. Fear has been fueled by

stories of hackers breaking into merchant web sites, collecting details for a

large number of credit cards and using this information to defraud card payment

systems. Stories also abound of people receiving erroneous bank statements, or

of fake ATMs being installed on high streets and in shopping malls to capture

PIN and the debit card details. The fact

that no viable and ready-to-market bank solutions are in sight only stimulates

this decline in the confidence of buyers.

In a recent informal meeting, it was pointed out that based

on a leading credit card organization’s transactions, 90+% of mail order and

telephone order fraud in Europe is Internet based. 15% of Internet clearing

volume is charged back while 50% of digital goods purchased over the Internet

are charged back. The solution, and the challenge, is to devise a way to use

this insecure environment while retaining all the advantages of the proven and

secure EFTPOS network.

The Internet Identification Requirements

To give organizations the confidence to reveal corporate

secrets, divulge privileged client information or grant access to powerful

transaction processing capabilities means it is essential to be able to trust

that people on the Internet are indeed who they claim to be. Furthermore, the

growth of one-to-one marketing has focused marketing strategies on segmenting

the client based down to one. To be

confident that access has been granted to the proper authorized party demands a

solution that can:

![]() Assure the authenticity of the

employee or client

Assure the authenticity of the

employee or client

![]() Assure the confidentiality of

privileged information

Assure the confidentiality of

privileged information

![]() Assure the integrity of data

Assure the integrity of data

![]() Assure the irrefutability of the

transaction

Assure the irrefutability of the

transaction

Internet Payment Security Requirements

The Internet is a user-friendly and open environment. For a

payment solution to be successful, it must maintain this ease and openness

without putting the current EFTPOS network at risk. This means finding a

payment transaction solution that can establish trust between buyer and seller

by addressing the following security issues:

![]() Authenticity of the buyer and the

seller

Authenticity of the buyer and the

seller

![]() Veracity through the use of PIN of the

identity of the card user

Veracity through the use of PIN of the

identity of the card user

![]() Confidentiality and privacy of

information relating to content of the Transaction

Confidentiality and privacy of

information relating to content of the Transaction

![]() Integrity of transmission data

Integrity of transmission data

![]() Irrefutability of the transaction.

Irrefutability of the transaction.

Nevertheless, to be completely successful, the Internet

payment system must also be capable of dealing with the following additional

issues:

![]() Guaranteed payment upon fulfilled

terms of delivery

Guaranteed payment upon fulfilled

terms of delivery

![]() Mobility that allows the buyer to

conduct business on the Internet from any point of interaction, regardless of

the device type or location

Mobility that allows the buyer to

conduct business on the Internet from any point of interaction, regardless of

the device type or location

![]() Support for an array of existing

payment products

Support for an array of existing

payment products

![]() Incorporation of an effective (i.e.

economical) micro-payment system

Incorporation of an effective (i.e.

economical) micro-payment system