Each day I receive a variety of articles on the subject of mobile payments and find countless opinions about the evolution, risks and capabilities of mobile payments.

As is always good form a definition is in order. I could begin by suggesting a mobile payment is any time that while moving about I can purchase something from someone using some recognised means of payment or currency. So at the most basic level of understanding carrying cash in our pockets was and still remains a form of mobile payments. Yet this is not what we mean when we discuss mobile payments. What we have done is combined two words from two worlds into a new thought. Mobile emerging from the arena of telephony and the use of the concept of a phone that does not need to be connected with a piece of wire. Wireless, cellular and mobile all are terms that we associate with the use of radio waves to connect a telephone to a network allowing us to make phone calls from someplace that is in proximity to a receiver or cell tower or satellite. Now I’m sure all of my readers know these things and are wondering what is the point.

The point is that we also talk about contact-less payments that concept of waving a card in front of an antenna, thus allowing the card to receive power through induction and then communicate with the device controlling the antenna. Some people call it that “Tap and Go” feeling others refer to it a PayPass, Visa Wave, Express Pay card and if we travel the world we will find an assortment of other brand names such as Dexit. In many cities transit agents discovered that by employing contact-less cards interfacing with – terminals they could create efficiencies, improve information about ridership and maybe even reduce fraud.

So now we have to discuss the application of the technology. This brings us to the idea of closed loop and open loop systems. Neither are new thoughts, charge cards issued by department stores are closed loop they only work at that companies stores. Open loop refers to systems that are widely accepted because someone has gone out and branded a concept, convinced merchants it is convenient and then offered a “Card” to you and I so that we can be identified and employ this “Means of Payment”. Classic brands that we think of as Open Loop systems include money, MasterCard, Visa, Interac, PIN, eurocheque and an assortment of national brands.

Yet all of these systems have inherent inefficiencies. Inefficiencies that some see as benefits and others see as highway robbery. Then there is that class of people who enjoy getting something for “nothing” they like the idea of counterfeiting money, replicating credit and debit cards, capturing our PIN and ultimately stealing our identity and more importantly our hard earned money. I could also mention merchant discounts, late fees, interest charges, interchange but those are all for another day.

The operators of these systems understand or learn about these various methods of “Stealing” identity and money and have built systems to mitigate the risk, eliminate no minimize yes. In Europe and throughout the world (except the USA) the members of MasterCard, Visa and the various domestic systems are working to reduce these threats by introducing Smart Cards or Chip Cards all cards employing the EMV specification that have a computer embedded within. The benefit is that PIN can easily be introduced on credit cards, the cost of telecommunications can be reduced by allowing the computer in the card to make intelligent decisions when ever that card is used to effect a payment.

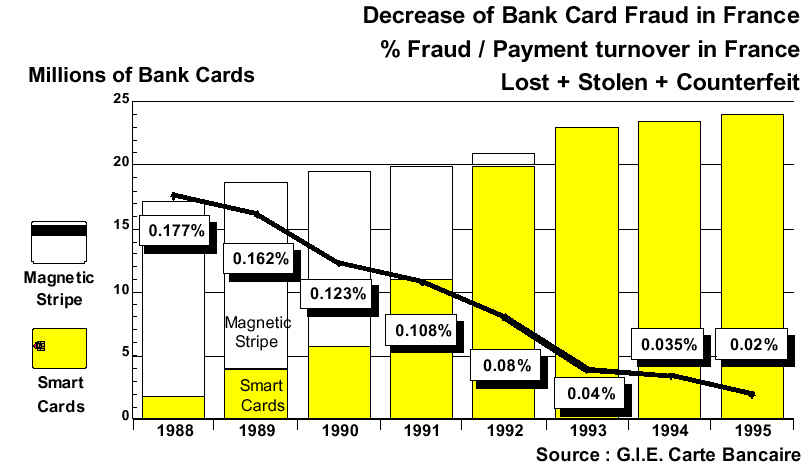

This movement to secure payment cards with the technology and specifications defined within the EMV specifications began first in France where they went out on their own developed their own specifications and proved to the world that smart cards or chip cards can and will reduce the level of card present fraud and can if employed properly also reduce the cost of telecommunications. their success can easily be seen in this chart that tracked their progress and success.

![]()

Remarkable success, yet they were now faced with an issue. First the criminals understood if they disabled the chip (computer) the merchant could still swipe the card and read the magnetic stripe. This one easily could be solved by eventually not allowing cards that should have a chip to be swiped through the magnetic stripe reader. But what about when these cards were used in Holland, England or anywhere that had not, and at the time no one had, adopted the same means of defense. The net result fraud migrated from being a domestic issue to the cards being used in neighboring countries. Obviously the French became proponents of a global migration to smart cards and convinced Visa, MasterCard and Europay to develop the EMV specifications, recognising that they would have to eventually convert.

I could continue to digress from my main theme and talk about how each country went through its decision making process. I could then go on and talk about how far along they are in their implementations. Suffice it to say some are finished, others are diligently working towards completion and others are moving at a pace that does not cause undue expense and allowing natural replacement cycles to drive the timescale for implementation.

Here in the country where I live they also have a Chip Migration strategy. Canada is inpilot or a trial depending on how the lawyers interpret the efforts of banks potentially colluding together. By the summer cardholders in the Kitchener Waterloo area will be using these chip cards and the media, banks, merchants, processors and associations will be monitoring and learning how the Canadian’s feel about and their willingness to embrace the change.

The following chart outlines Interac’s schedule for deployment. MasterCard is playing along without committing. Whereas Visa has stated that they will push the liability for fraudulent transaction not protected by EMV to the Acquirer if their merchants are not compliant by October of 2010.

So how does all of this affect the introduction of Mobile Payments or Contact-less Cards. A mobile payment is simply, today, a contact-less payment performed using a mobile phone with the contact-less interface inside as apposed to to using the card as the form factor.. Well some will say not at all, the drivers are different the business case is not the same. Yet the core technology is a computer in the card. So why worry, eventually all of this could come together. Or will the USA decide to take another path all together.

So to end this particular blog I ask a simple question, based on the premise that the mobile and contact-less payments that we see emerging are all about speeding up low value <$25 dollar transactions. What happens when I want to use my contact-less mobile phone for a payment for say a $1,500 hotel bill. Will I tap my contact-less device “mobile phone”. Have to find a place to put it while I either enter my PIN or sign the receipt. Today the clerk typically holds the card for me while I sign the receipt tomorrow what. Or will they decide to merge contactless and EMV creating a more interesting problem. I’ll need to keep that phone near the antenna while my PIN is verified and the transaction is authorized.

Or should we go on and talk about the security concerns that everyone has described in countless articles and numerous logs. The idea that the criminal will walk down the street reading the content of your purse or wallet with their hidden antenna.

Or should we talk about who is going to pay the price of adding the contact-less antenna to the merchants point of sale equipment.

Let me hold those for another day and another flow of thought.

![]()

Hey!! I am thoroughly impressed with your knowledge of Bill Of Sale. Your insights into this article about Bill Of Sale was well worth the the time to read it. I thank you for posting such awsome information. Signed James Kryten on this Day Friday.